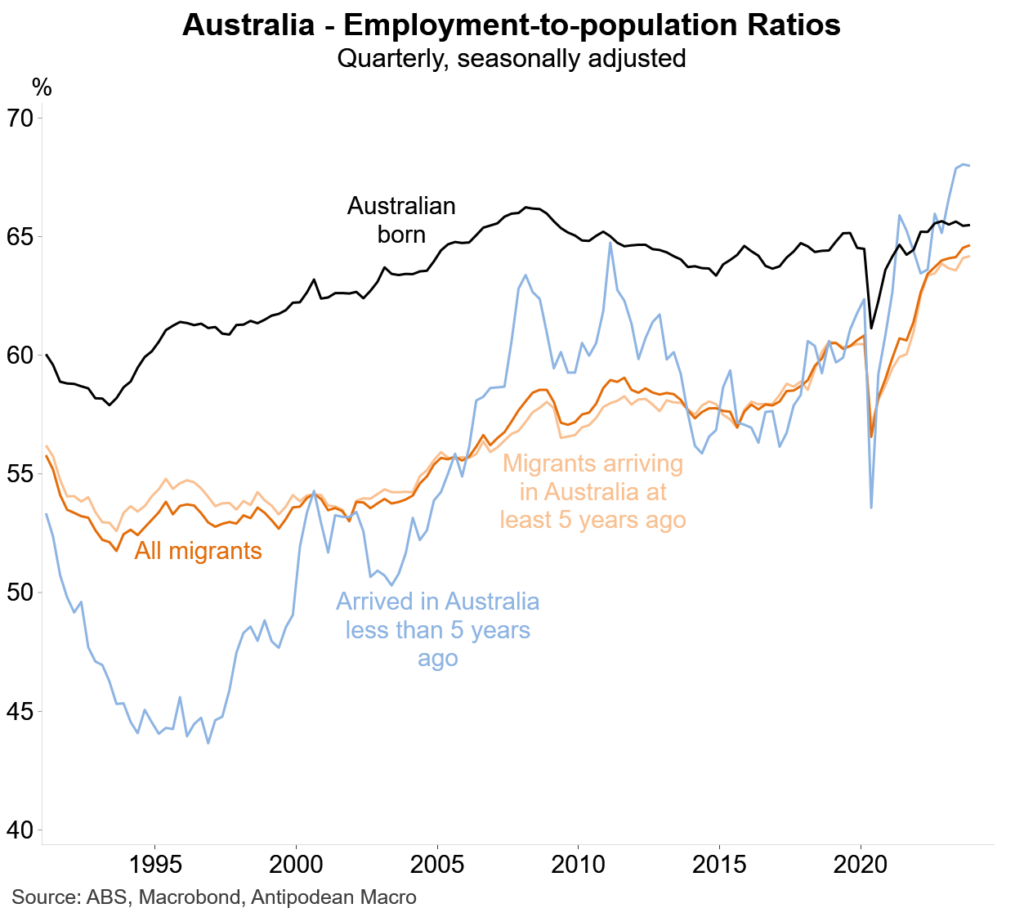

1. More migrants…

The share of the Australian-born population aged 15+ in employment is lower than the peak prior to the GFC. In part this reflects the aging of our population weighing on labour force participation. Interestingly migrants’ employment-to-population ratio in aggregate has risen significantly over time, and since pre-COVID.

Source: ABS, Macrobond, Antipodean Macro (February 2024)

Source: ABS, Macrobond, Antipodean Macro (February 2024)

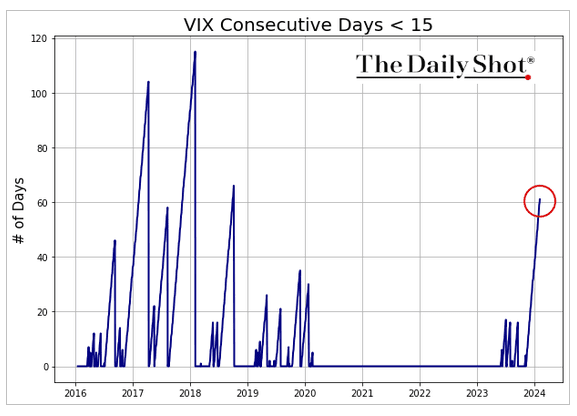

2. All calm on the 2024 front…

If it feels a little calmer than usual, that may be because the VIX has been below 15 for 61 trading sessions in a row. This hasn’t happened for over 5 years.

Source: The Daily Shot (February 2024)

Source: The Daily Shot (February 2024)

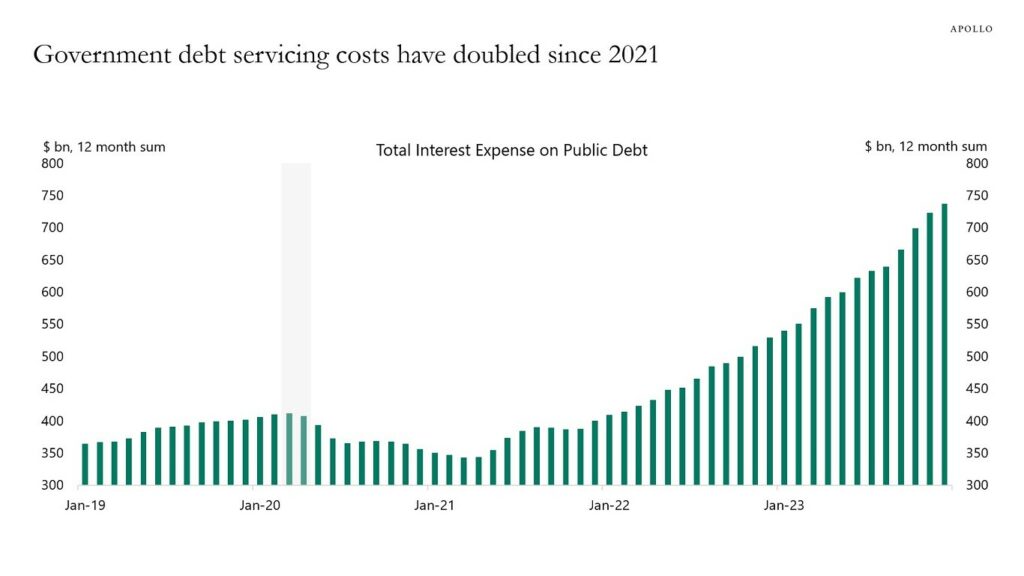

3. The cost of credit…

US government annualised debt servicing costs are over $700 billion due to increased interest rates and debt levels. In 2021 they were around $350 billion.

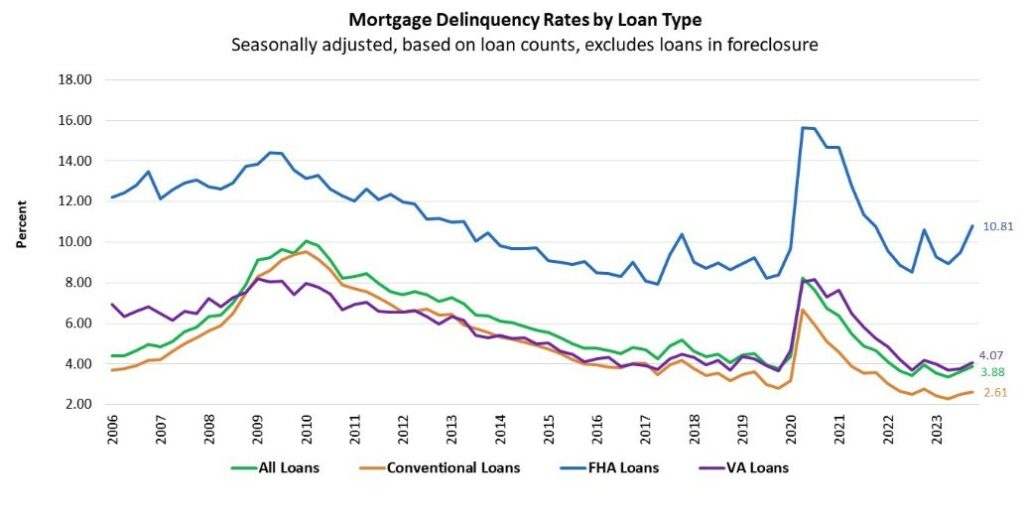

According to the US Mortgage Bankers Association, mortgage delinquencies increased across all product types for the 2nd consecutive quarter, and the pace of new loans entering delinquency has picked up.

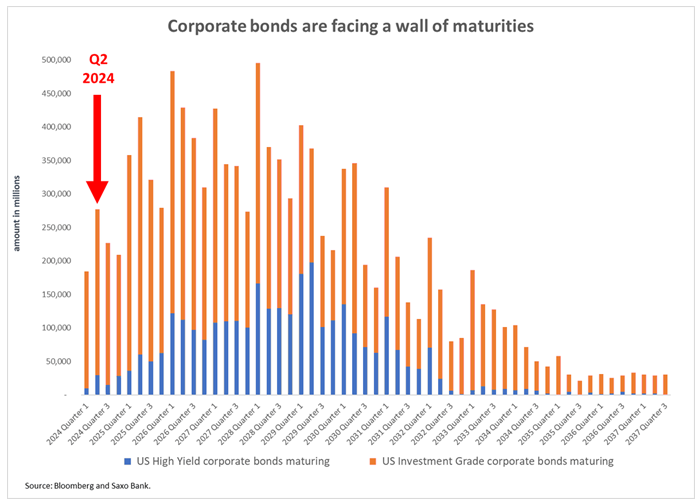

Roughly $276 billion of corporate bonds (Investment Grade + High Yield) need to be refinanced in Q2 2024. HY must refinance from an average coupon of 5.8% to 9%. IG must refinance from an average coupon of 3.77% to 5.75% – the highest since Q3 2007, according to Evans.

Source: Apollo (February 2024)

Source: Apollo (February 2024)

Source: Mortgage Bankers Association (February 2024)

Source: Mortgage Bankers Association (February 2024)

Source: Bloomberg and Saxo Bank (February 2024)

Source: Bloomberg and Saxo Bank (February 2024)