1. Are we summitting…

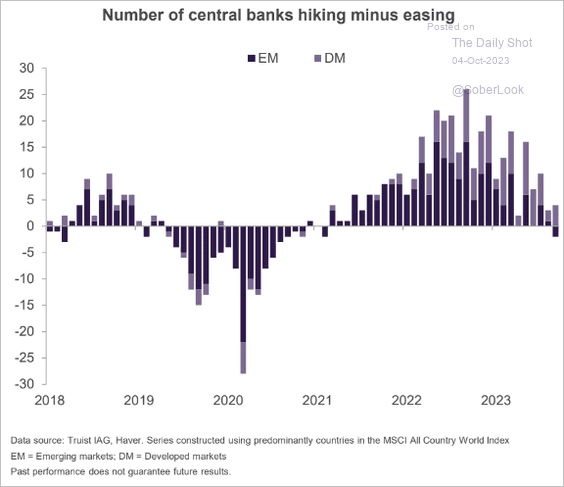

Everyone is trying to call the end of the global rate hiking cycle. This chart is an interesting representation of central bank sentiment. The number of central banks hiking minus easing has hit negative territory in Emerging markets and is approaching zero in developed markets.

San Francisco Fed President Daly was the latest official in the US to strongly suggest the US was done with its rate hikes this week.

Source: Truist IAG, Haver (October 2023)

Source: Truist IAG, Haver (October 2023)

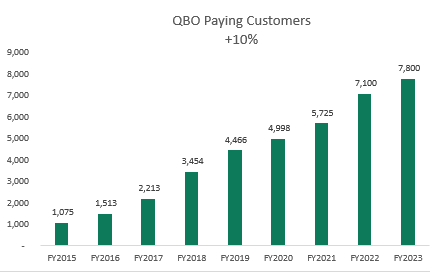

2. We are still Intuit (!)…

Intuit, held in the S3 Global Opportunities Fund, held their investor day recently with a strong update on key metrics. We were pleased to see QuickBooks added +10% customers in the year, with average revenue per customer growing +16%. Intuit have strong customer retention and are able to capture greater share of customer wallets by adding additional services into their offering, like payments (where volumes were +18%) and payrolls (volumes grew +9%), all in the face of tougher economic conditions.

Source: Firetrail, Intuit (October 2023)

Source: Firetrail, Intuit (October 2023)

Source: Firetrail, Intuit (October 2023)

Source: Firetrail, Intuit (October 2023)

Companies mentioned are illustrative only and not a recommendation to buy or sell any particular security.

3. Hasta la vista Euro…

Interesting data on SWIFT international payments has shown a ‘de-euroisation’ is happening. The Euro share of global SWIFT payments has dropped to 23%, from 38% at the start of the year. Whilst the proportion of Foreign Exchange payments involving the USD hit an unprecedented 46% in July, according to Bloomberg.

China’s Yuan is also on the rise. China’s share in SWIFT payments hit an all-time high of 3.47% in August. The Yuan represented 5.4% of Brazil’s international reserves at the end of 2022, the second-largest share surpassing the Euro, according to the Central Bank of Brazil. And after several Russian banks were kicked out of SWIFT as part of Western Sanctions, they are increasing their Yuan trade.

Source: Bloomberg, Jeroen Blokland (October 2023)

Source: Bloomberg, Jeroen Blokland (October 2023)