1. Beats, builders and buybacks…

Homebuilders had a strong week of performance after March US housing starts beat estimates. Housing starts were -0.8% m/m (vs -3.5% expected) and single family starts were +2.7% m/m.

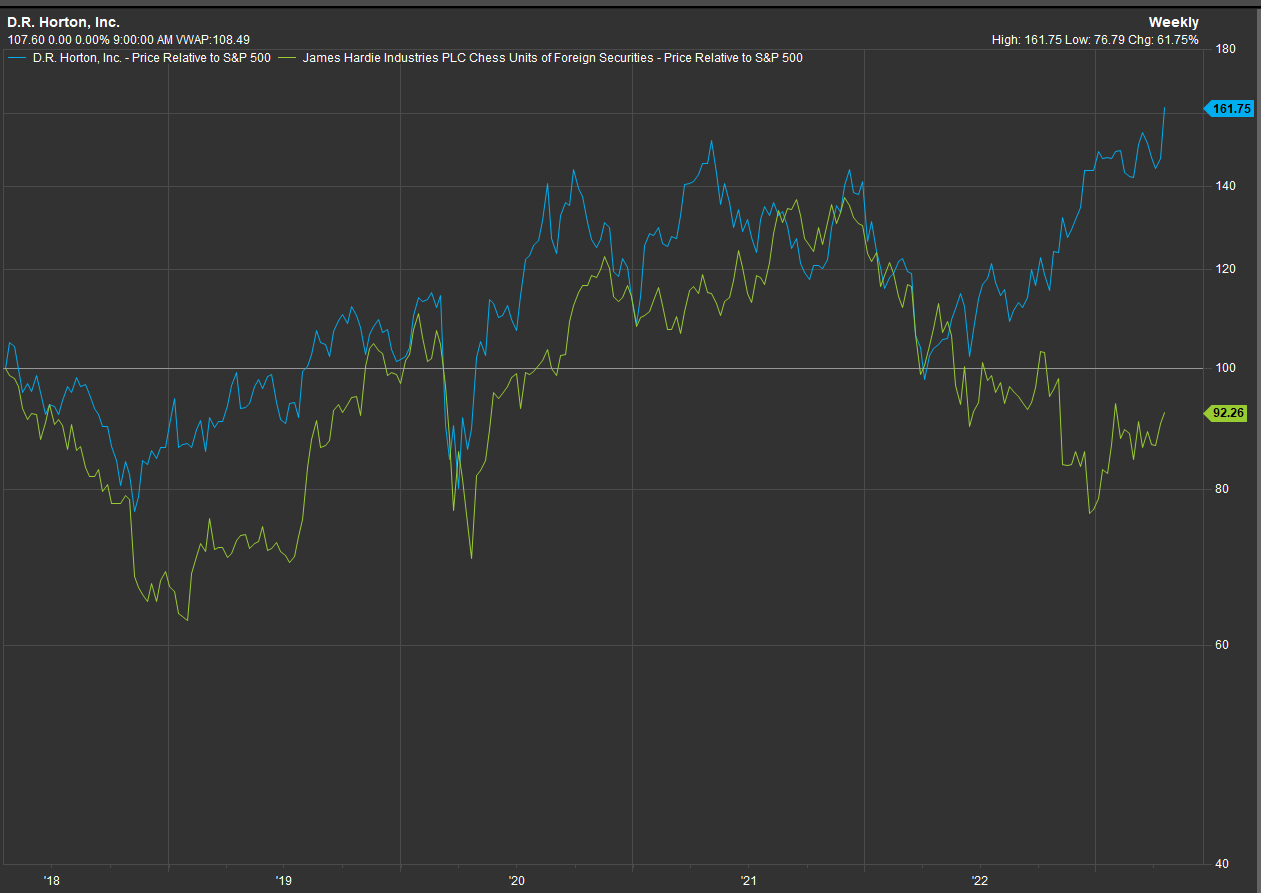

Following the ‘better than expected’ data, the largest home builder in the US beat expectations last night, DR Horton. The builder said “we see much more stability in both cost and demand and deliveries and margin“. DR Horton is the largest customer of Aussie portfolio holding James Hardie.

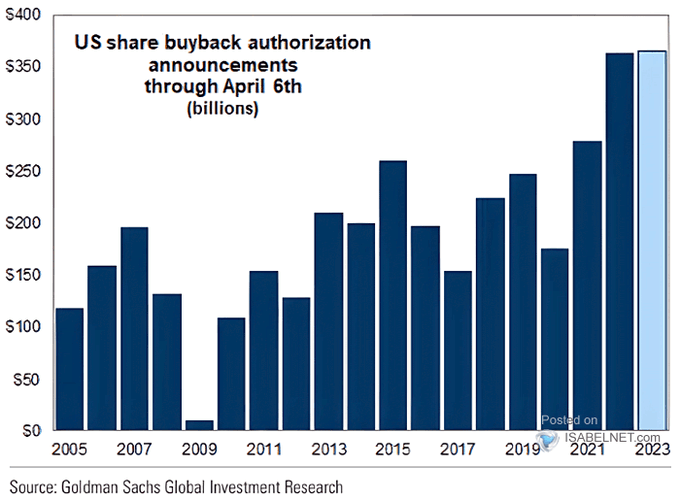

And we are keeping a close watch on the buyback announcements that accompany the results. 2023 has been a big year so far, see chart below.

DR Horton (blue) vs James Hardie (green) share price performance

Source: Factset

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

2. Consumer care…

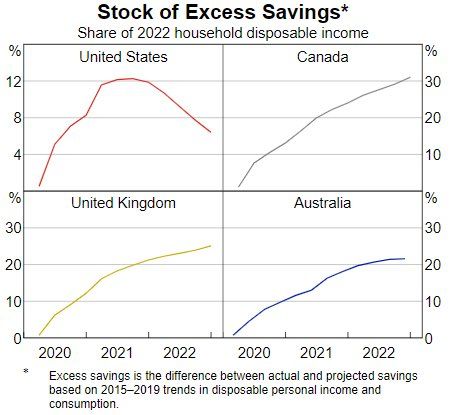

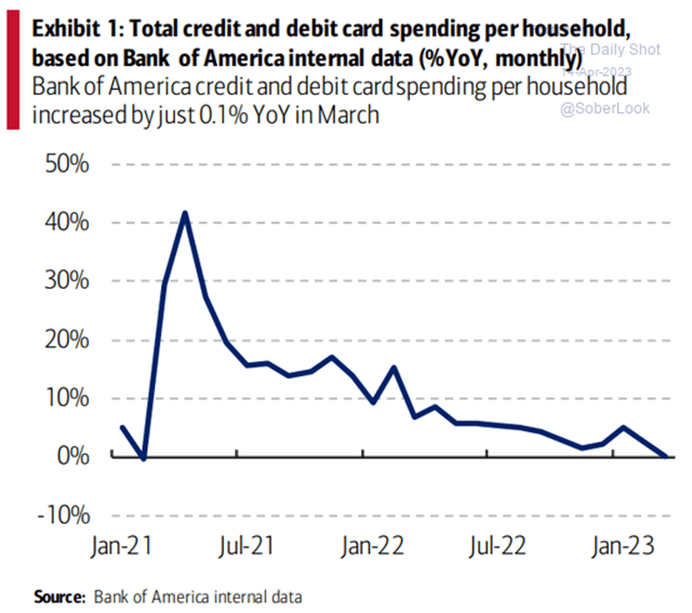

All eyes remain on how the global consumer is faring. See a collection of graphs below which show:

- Australia’s excess savings have started to plateau, while the US has dropped sharply.

- The credit card has been put securely back in the holster in the US, with BoA data showing credit and debit card spending increased by just 0.1% y/y in March

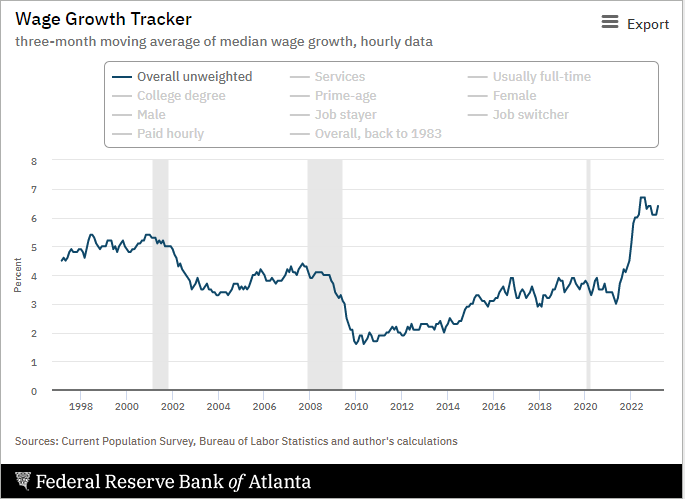

- In the US, the Atlanta Fed’s wage growth tracker has accelerated in March to 6.4%, from 6.1% in February. But looks like it’s starting to flatline at those levels.

Source: Evans

Source: Evans

Source: Bank of America internal data

Source: Current Population Survey, Bureau of Labor Statistics and author’s calculations

3. On the road again…

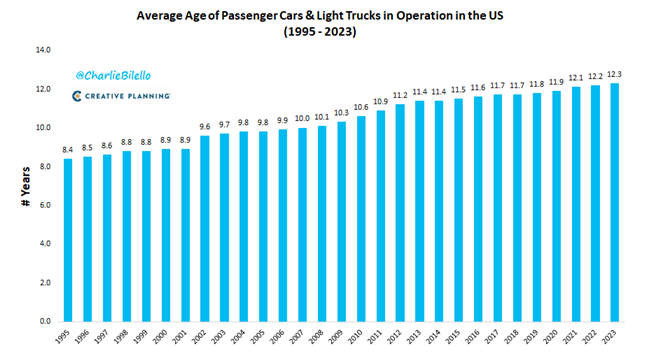

Despite the EV hype, the average age of US cars continues to rise. This is benefitting S3 Global Opportunities Holding AutoZone, who is one of the leading retailers and distributors of automotive replacement parts in the US.

Source: Barrenjoey

Source: Barrenjoey

Companies mentioned are illustrative only and not a recommendation to buy or sell any particular security.