1. What’s in store for 2024…

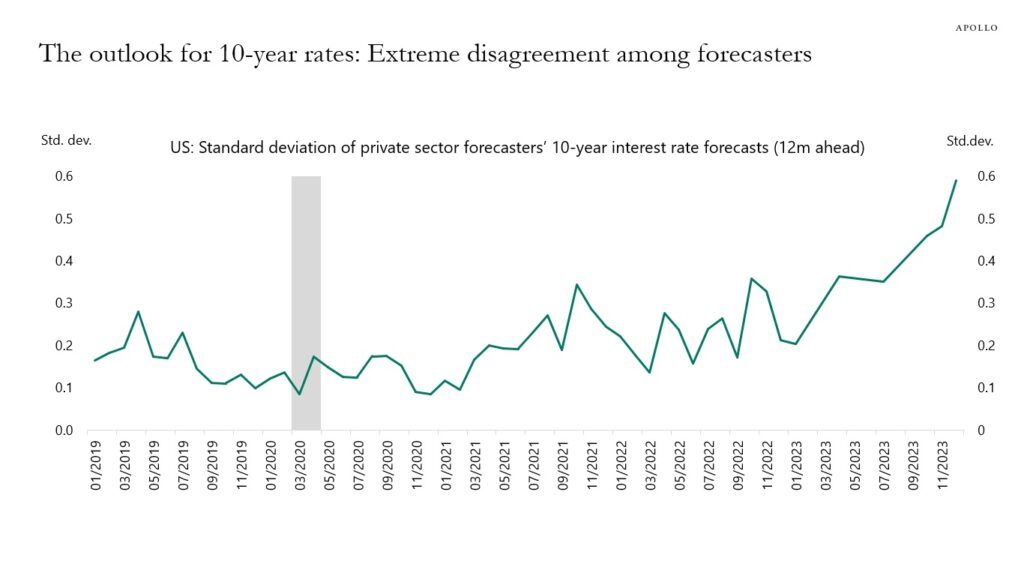

As we kick off 2024, the Bloomberg US Financial Conditions are at their loosest level since before the Ukraine invasion, suggesting the macro environment is supportive. But the level of disagreement on the outlook for long-term interest rates is surging up (measured by the standard deviation of forecasts for the US 10-year rate in 12 months’ time). Forecasts range from a US 10-year rate at the end of 2024 above 5%, down to below 3%.

Meanwhile Fund Managers are the most bullish they have been in 2 years!

Source: Bloomberg (January 2024)

Source: Bloomberg (January 2024)

Source: Bloomberg, Apollo Chief Economist (January 2024)

Source: Bloomberg, Apollo Chief Economist (January 2024)

Source: BofA Global Fund Manager (January 2024)

Source: BofA Global Fund Manager (January 2024)

2. The housing horror rolls on…

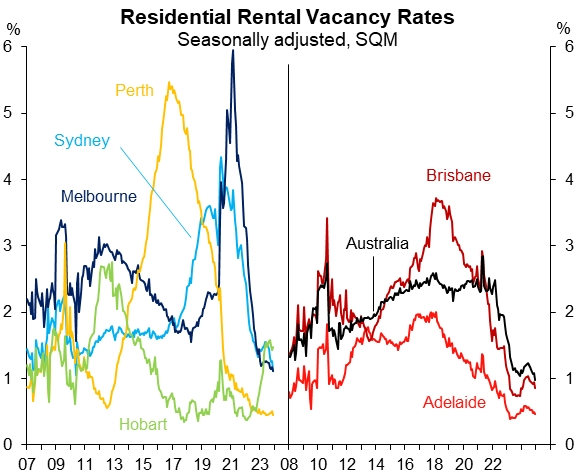

SQMs residential rental vacancy rates have declined to new lows across Sydney and Melbourne.

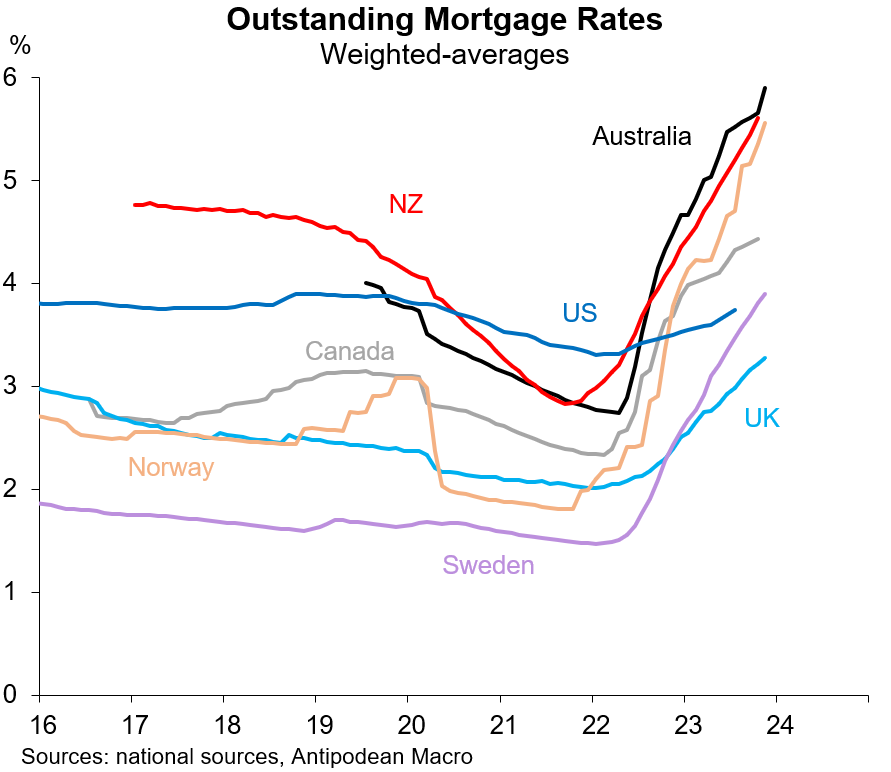

Meanwhile the average outstanding mortgage interest rate in Australia is higher than most other major economies.

Source: SQM Research (January 2024)

Source: SQM Research (January 2024)

Source: National Sources, Antipodean Macro (January 2024)

Source: National Sources, Antipodean Macro (January 2024)

3. No bottom to the barrel…

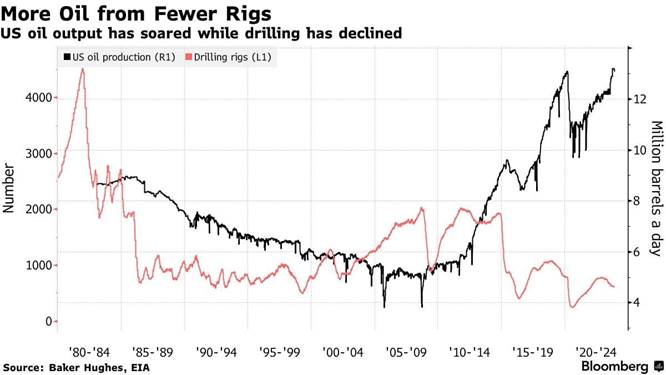

In 2023 the US produced more oil (per day) than any other country has ever produced. Whilst the number of drilling rigs continued to decline.

Standard Chartered have predicted that oil demand will increase in 2024 by 1.54 million barrels per day (b/d), and by 1.41 million b/d in 2025, above historical trend levels. Standard Chartered, and the EIA, expect little incremental oil supply in 2024.

Source: Baker Hughes, EIA, Bloomberg (January 2024)

Source: Baker Hughes, EIA, Bloomberg (January 2024)